All Categories

Featured

Table of Contents

[/image][=video]

[/video]

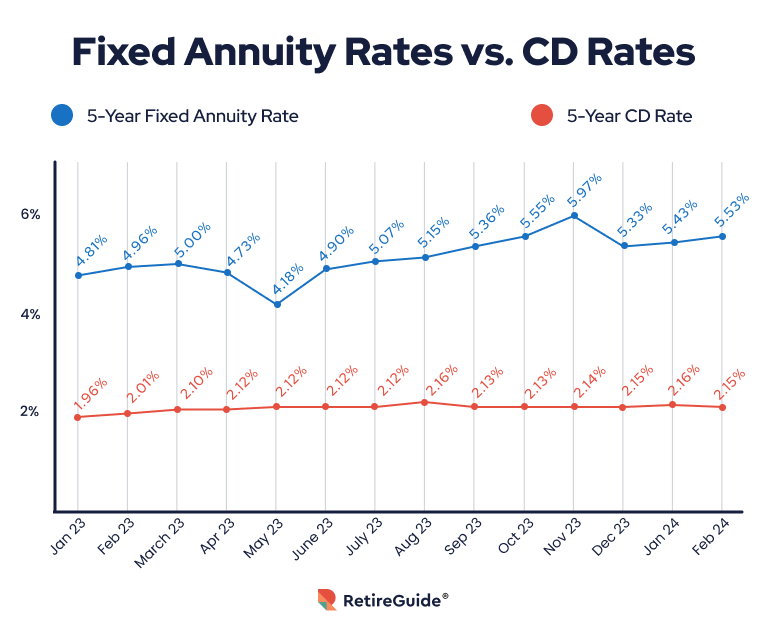

Multi-year ensured annuities, also referred to as MYGAs, are repaired annuities that secure a steady rates of interest for a defined time duration. Surrender periods normally last three to ten years. Because MYGA prices transform daily, RetireGuide and its partners update the following tables listed below frequently. It is very important to check back for the most current details.

Numerous elements identify the price you'll get on an annuity. Annuity prices have a tendency to be higher when the general degree of all rate of interest is higher. When purchasing fixed annuity rates, you may locate it useful to compare prices to deposit slips (CDs), an additional popular choice for secure, reputable development.

As a whole, set annuity rates outpace the rates for CDs of a similar term. In addition to gaining a greater rate, a dealt with annuity may supply better returns than a CD due to the fact that annuities have the advantage of tax-deferred growth. This means you won't pay taxes on the rate of interest made till you begin receiving settlements from the annuity, unlike CD passion, which is counted as taxed earnings every year it's gained.

This led lots of specialists to think that the Fed would certainly reduce rates in 2024. Nevertheless, at a plan forum in April 2024, Federal Book chair Jerome Powell recommended that prices may not boil down for a long time. Powell stated that the Fed isn't sure when rates of interest cuts could happen, as inflation has yet to drop to the Fed's criteria of 2%.

Integrity Annuity

Bear in mind that the very best annuity rates today might be various tomorrow. It is very important to talk to insurer to validate their specific rates. Begin with a totally free annuity assessment to find out how annuities can assist money your retirement.: Clicking will take you to our partner Annuity.org. When contrasting annuity prices, it's important to perform your very own study and not entirely pick an annuity simply for its high rate.

Take into consideration the kind of annuity. Each annuity kind has a various variety of average interest rates. As an example, a 4-year set annuity might have a greater price than a 10-year multi-year guaranteed annuity (MYGA). This is because dealt with annuities could use a greater rate for the very first year and afterwards decrease the rate for the remainder of the term, while MYGAs guarantee the price for the entire term.

The guarantee on an annuity is just comparable to the company that releases it. If the company you buy your annuity from goes damaged or bust, you could shed money. Check a firm's monetary strength by consulting across the country acknowledged neutral ranking firms, like AM Ideal. A lot of professionals suggest only thinking about insurance firms with a score of A- or over for long-term annuities.

Annuity income climbs with the age of the buyer since the income will certainly be paid out in less years, according to the Social Safety Management. Don't be stunned if your price is higher or less than a person else's, even if it's the exact same item. Annuity rates are simply one factor to think about when getting an annuity.

Recognize the costs you'll need to pay to provide your annuity and if you need to pay it out. Squandering can set you back up to 10% of the worth of your annuity, according to the Wisconsin Office of the Commissioner of Insurance policy. On the other hand, management costs can include up over time.

Tiaa Cref Lifetime Annuity

Inflation Rising cost of living can consume up your annuity's worth over time. You might take into consideration an inflation-adjusted annuity that improves the payments over time.

Check today's listings of the very best Multi-year Surefire Annuities - MYGAs (upgraded Thursday, 2025-03-06). These lists are arranged by the surrender cost duration. We modify these listings daily and there are frequent modifications. Please bookmark this web page and come back to it usually. For expert aid with multi-year guaranteed annuities call 800-872-6684 or click a 'Obtain My Quote' switch beside any kind of annuity in these checklists.

Deferred annuities enable an amount to be withdrawn penalty-free. Deferred annuities typically enable either penalty-free withdrawals of your made passion, or penalty-free withdrawals of 10% of your contract worth each year.

The earlier in the annuity duration, the greater the penalty percent, described as surrender fees. That's one reason why it's finest to stick to the annuity, as soon as you devote to it. You can pull out every little thing to reinvest it, but prior to you do, make certain that you'll still prevail that method, even after you figure in the abandonment charge.

The surrender charge might be as high as 10% if you surrender your agreement in the very first year. Oftentimes, the surrender cost will decrease by 1% each contract year. An abandonment cost would be billed to any type of withdrawal higher than the penalty-free quantity enabled by your postponed annuity contract. With some MYGAs, you can make very early withdrawals for emergencies, such as wellness expenditures for a severe disease, or confinement to a retirement home.

You can set up "methodical withdrawals" from your annuity. Your various other option is to "annuitize" your deferred annuity.

Present Value Of Annuity Due Chart

This opens a range of payment alternatives, such as earnings over a single life time, joint lifetime, or for a specific duration of years. Many delayed annuities permit you to annuitize your agreement after the initial contract year. A significant difference is in the tax obligation treatment of these products. Passion made on CDs is taxable at the end of every year (unless the CD is held within tax competent account like an IRA).

The passion is not exhausted until it is eliminated from the annuity. In other words, your annuity expands tax obligation deferred and the passion is compounded each year.

Inheritance Tax On Annuities

You have numerous choices. Either you take your money in a round figure, reinvest it in one more annuity, or you can annuitize your agreement, converting the round figure into a stream of revenue. By annuitizing, you will only pay tax obligations on the interest you receive in each payment. You have 30 days to inform the insurance policy company of your intentions.

These features can differ from company-to-company, so make sure to discover your annuity's survivor benefit features. There are a number of advantages. 1. A MYGA can suggest reduced tax obligations than a CD. With a CD, the interest you earn is taxable when you earn it, even though you don't receive it up until the CD matures.

At the very the very least, you pay taxes later, instead than faster. Not only that, yet the intensifying interest will be based on an amount that has not already been strained. 2. Your recipients will certainly obtain the full account worth since the date you dieand no abandonment fees will certainly be deducted.

Your beneficiaries can select either to receive the payment in a round figure, or in a collection of income repayments. 3. Usually, when somebody passes away, even if he left a will, a court chooses who gets what from the estate as in some cases loved ones will argue regarding what the will means.

With a multi-year fixed annuity, the owner has plainly marked a recipient, so no probate is called for. If you add to an IRA or a 401(k) strategy, you obtain tax obligation deferral on the earnings, just like a MYGA.

{kind=link}

Latest Posts

The Best Ways To Maximize Your Retirement Income In 2025

Neap Annuity

State Of New Jersey Teachers Pension And Annuity Fund